— By Dan Diehl —

Navigating the digital transformation of building products and services.

The building products, services and solutions industry is being transformed. Like many industries before it, the market for commercial building products, services and solutions (BPSS) is undergoing a digital transformation. This sector has been a relative innovation laggard for several reasons, including: the long life cycles of buildings and major building systems; the fact that each building is somewhat unique, requiring engineered systems; and the win/lose legacy culture that traces its roots to the hardball construction industry.

Dan Diehl, Aircuity.

Nevertheless, we believe the market is being transformed, and that the pace of change is accelerating. In this article we share our view on how the transformation is likely to play out, and which companies are most likely to succeed in the new environment. Are there companies poised to become the Googles, Amazons or Salesforces of the BPSS industry? What strategies or business models will the successful companies adopt?

Transformation Patterns in Other Industries

In many of the early digital transformations, innovators used web technology to improve upon the way things had been done in a given industry. Amazon made it easier to find and purchase a book or CD. Netflix made it easier to rent DVDs through the mail with an innovative subscription model. Salesforce made it simpler to adopt CRM software via its pioneering SaaS (Software as a Service) model.

As the digital revolution has evolved, and the technologies have advanced, a second phase of innovation has seen successful companies fundamentally redefine entire industries, with new value propositions, new business models and new cultures. Amazon has become a retail platform that leverages crowdsourced customer reviews, uses analytics to predict what each customer wants, and enables third-party sellers alongside its own offerings. Netflix migrated to streaming, becoming the dominant player, and is now using its massive customer data set to design original programming that will appeal to specific segments of viewers. Salesforce has become a business solutions platform, branching out from CRM to include service management, and introducing its Lightning platform that allows customers and third-party developers to more easily customize or create applications. As discussed below, the winners of the BPSS digital transformation will develop these kinds of Phase II solutions that redefine the industry.

Forces Driving Change in BPSS

Several factors are accelerating the pace of change in BPSS:

- Customers are dissatisfied with legacy vendor solutions that don’t deliver and demonstrate compelling value. For example, in many situations, services are being sold as the “what?” (scheduled on-site, truck roll-based PM services) and the “how?” (delivery of ‘hours’ as a commodity and check-the-box task completion) rather than the “why?” (increased uptime reliability, sustained levels of occupant experience). But progressive buyers of services are increasingly less willing to pay for BAS or chiller service agreements that are based on labor rates and hours. They are much more willing to pay for performance, tying service fees to verified outcomes, such as critical equipment uptime.

- Customers’ expectations have been raised by the innovative, responsive and customer friendly companies they deal with in other parts of their business and personal lives (Salesforce, Amazon, Uber, etc.).

- SCADA systems are commoditizing BAS offerings and eroding the “lock-in” power of their proprietary products.

- ASHRAE is helping drive the adoption of open protocols and metadata definitions with its proposed standard 223P, announced in February 2018.

- The combination of IoT, big data, cloud-based platforms and analytics are undermining the value and profitability of legacy products and services, while simultaneously enabling higher value, more profitable solutions.

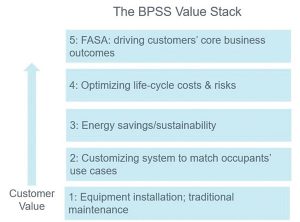

Moving Up the Value Stack: Facilities as Strategic Assets

In response to commoditization and changing customer expectations, the new technologies are first being used to make existing service models more efficient. Instead of sending a BAS or HVAC technician to do a preventive inspection, or to troubleshoot a problem, forward-thinking solution providers are using remote monitoring and analytics to perform those tasks more effectively and at lower cost. New technologies also allow them to demonstrate the value they are creating by documenting critical outcomes, including equipment uptime, space conditions (including IEQ) and energy consumption. This approach is still somewhat innovative, but it will rapidly become table stakes, the standard for doing business at the bottom of the BPSS value stack.

Further up the value stack are solutions that leverage data and analytics to provide guaranteed service level agreements (SLAs), in which the customer pays a variable fee based on verified outcomes achieved and sustained. Another set of higher value offers will be based on life cycle management and long term asset planning. For example, a solution provider may guarantee the 10-year life cycle costs of a chiller, and take responsibility for installation, continuous commissioning, maintenance, any required rebuilds, cooling and energy performance and financing. Or the service company may own the chiller and related equipment, providing chilled water as a service.

Further up the value stack are solutions that leverage data and analytics to provide guaranteed service level agreements (SLAs), in which the customer pays a variable fee based on verified outcomes achieved and sustained. Another set of higher value offers will be based on life cycle management and long term asset planning. For example, a solution provider may guarantee the 10-year life cycle costs of a chiller, and take responsibility for installation, continuous commissioning, maintenance, any required rebuilds, cooling and energy performance and financing. Or the service company may own the chiller and related equipment, providing chilled water as a service.

At the top of the value stack are solutions based on an approach that we call FASA, or Facilities as Strategic Assets. The vendors and customers who adopt this approach view facilities as strategic assets that must be managed to drive the success of the customer’s core business. Their goal is to manage the design, maintenance, operation and retrofitting of buildings to measurably improve business (not just building) outcomes.

Similar to the pattern in other industries, the solutions higher up in the BPSS value stack will be enabled by a flexible value-creation ecology based on digital platforms that collect, analyze and learn from building and business data.

FASA Strategies Focus on Vertical Markets

Because FASA solutions start with critical business outcomes, FASA vendors must develop a deep understanding of their customers’ businesses. This usually means focusing product development, marketing and sales on the high-priority needs of companies in vertical markets.

For example, a leading manufacturer of networking equipment negotiated a performance-based agreement, in which its HVAC service company is paid an annual fee to assure uninterrupted cooling availability for servers that perform mission-critical simulations. The agreement includes large financial penalties that the service company is charged in the event of an interruption. It is up to the service company to decide what strategies to employ to avoid such outages, i.e., the mix of maintenance, redundant equipment, remote monitoring, etc. There are no contractually scheduled truck rolls, task checklists or specified hours beyond an annual total system performance assessment. This outcomes-based, FASA agreement has benefitted both parties, expanding the value pie. The service company received a multi-year agreement at attractive margins, reflecting the responsibility they were taking on, and the business value they were delivering. The manufacturer enjoys largely uninterrupted operation of a critical business process and gained a true partner who understands its core business priorities, and actively “looks around corners” on its behalf.

The Industry Profit Pool Will Migrate Up the Value Stack

As has been the case in other industries, the BPSS profit pool will migrate away from the companies offering legacy products and services and to those offering higher value solutions. We believe FASA solutions will capture a large share of industry profits in the years ahead.

By their nature, FASA solutions are on the radar screen of C-level decision makers. Companies offering these solutions will sell at the C-level and have the opportunity to become trusted business partners. That can lead to long-term relationships in which a FASA vendor deploys its solutions across a customer’s entire facilities portfolio. This can streamline the procurement process, shorten the sales cycle and reduce the cost of sale — to the benefit of both parties.

Culture is Critical

In order to benefit fully from the evolution of FASA strategies, the cultures of vendor and customer organizations must also evolve. Some of the key assumptions and values that need to be revisited include:

An Abundance Mentality

Compared to the culture of Silicon Valley, many organizations and professionals in BPSS have a scarcity mentality, tending to view their business interactions as a zero-sum game. We believe that this is in part due to the legacy culture of the construction business and the design>bid>build process. Whether in new construction or retrofit projects, the procurement process often focuses first on cost instead of life cycle value. This creates perverse incentives for vendors to compete by cutting corners.

FASA strategies require an abundance or win/win mentality. The goal for vendors is to innovate to create new pools of value that can be shared between the vendor, the customer and other partners in the value ecology.

Role and Status of BPSS Vendors and Facilities Leaders

Another inhibitor of FASA innovation has been the legacy cultural assumption on both the vendor and customer sides that facilities is primarily a cost center to be minimized. This can create a self-fulfilling prophecy, in which C-level buyers fail to put FASA vendors and solutions on their radar screens and fail to engage their own facilities leaders as top-level contributors within their management teams.

There are opportunities for solution providers and facilities leaders on the customer side to enhance their standing as full partners in the success of the customer’s business, helping move the needle on critical business outcomes. By demonstrating that FASA strategies can create core business value, they will be seen as business leaders, and will earn full participation in the management of the business, not just the buildings.

Focus on Innovation, Learning and Operational Excellence: Profit is Not Purpose

In the era of big data and analytics, customers will have more and more information about the value of facilities-related products and services. Vendor strategies based on customers having incomplete information or based on lock-in to proprietary products will be less and less viable.

In this environment, sustainable profitability is best seen as the outcome of creating verifiable business value for customers. In strategy development and in day to day execution, the most successful companies won’t solve to profitability. They will solve to creating customer value in some unique, differentiated way, with a business model that allows them to capture a fair share of the value pie as profit.

Ultimately, that focus on creating unique business value for customers is the essence of the approach we are advocating, a compass that can guide solution providers and building owners as they navigate the digital transformation of the BPSS industry by developing FASA strategies.

— Dan Diehl is the CEO of Aircuity; Paul O’Malley is the owner of Paul O’Malley Associates, LLC, a strategy and execution consulting firm. Lou Ronsivalli, principal of GioVantage Strategies, LLC, contributed to this article.